Momentum Builds for Corporate ESG Disclosure and Assurance, Yet Reporting Inconsistencies Linger, Study Finds

Benchmarking Global Practice ↓

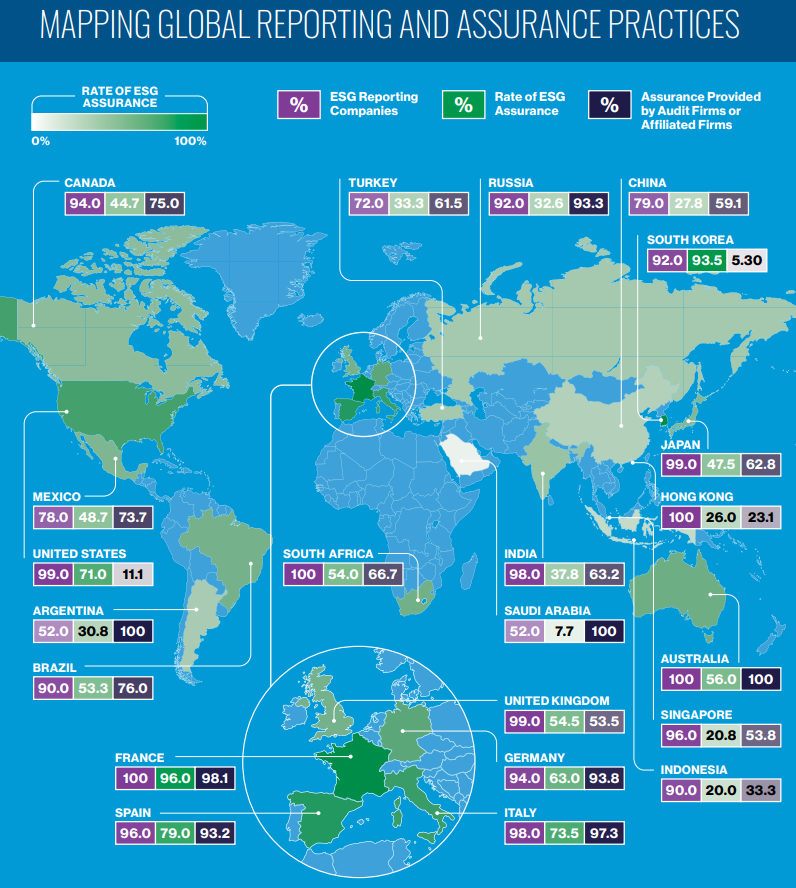

The largest global companies continue to show momentum on corporate reporting and related assurance involving environmental, social and governance (ESG) issues, according to a new report from the International Federation of Accountants (IFAC) and AICPA & CIMA, the latter two of which form the Association of International Certified Professional Accountants. Yet significant hurdles remain when it comes to providing consistent, comparable, and high-quality sustainability information for investors and lenders.

Some 95% of large companies reported on ESG matters in 2021, the latest year available, the IFAC-AICPA & CIMA study found. That’s up from 91% in 2019. Sixty-four percent of companies obtained assurance over at least some ESG information in 2021, up from 51% in 2019. The inability so far to coalesce around agreed upon global standards continues to create challenges, however.

“Even as we see companies increasingly report on ESG and sustainability, the data we’re tracking reveals continuing fragmentation around the world in terms of which standards and frameworks are used,” noted IFAC CEO Kevin Dancey. “Eighty-six percent of companies use multiple standards and frameworks. This patchwork system does not support consistent, comparable, and reliable reporting. Importantly, it also does not provide the necessary foundation for globally consistent, high-quality sustainability assurance.”

The report also examines the extent to which companies provide forward-looking information on emissions reduction targets and plans. While two-thirds of companies disclosed targets, they lag the rate at which companies report their historic greenhouse gas emissions (97%).

“Steady increases in reporting and assurance are significant, yet more companies need to take the additional step to obtain assurance to build trust and confidence in what they report,” said Susan Coffey, CPA, CGMA, AICPA & CIMA’s CE of public accounting. “The decision over who provides that assurance—and the rigor, skepticism and professional judgment they bring to the task—is critical.”

Additional Key Findings

♦Use of Sustainability Accounting Standards Board (SASB) standards and the Task Force on Climate-Related Financial Disclosures (TCFD) framework have increased significantly between 2019 and 2021: there was a 29% increase for SASB standards usage and 30% for the TCFD framework.

♦When companies obtained assurance from a professional accountant, they chose their statutory auditor 70% of the time.

♦Globally, the International Auditing and Assurance Standards Board's International Assurance Engagement Standard 3000 (Revised) remains the most popular standard when providing assurance.

95% of firms providing assurance use ISAE 3000, up from 88% in 2019.

38% of non-accountant service providers use ISAE 3000, up from 34% in 2019.

First, please LoginComment After ~